In the hyper-accelerated economic landscape of May 2026, the concept of a «savings account» has been radically redefined. We have moved past the era of passive accumulation into the age of Active Financial Engineering. In this environment, every dollar held in reserve must be treated as a precision instrument designed to protect purchasing power against a volatile market.

Mastering your wealth today requires more than just «setting money aside.» It requires a sophisticated Smart Yield Engine—an autonomous, high-performance system that balances immediate accessibility with maximum capital efficiency.

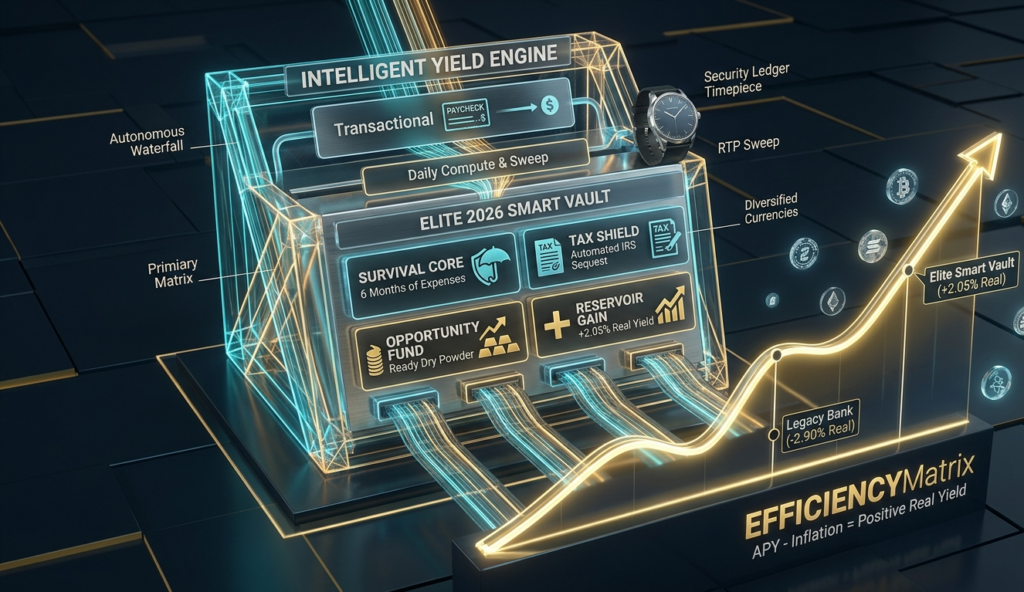

1. Quantitative Benchmarks: The Efficiency Matrix

In 2026, the cost of banking with a legacy institution is no longer measured just in fees, but in lost opportunity. To understand the stakes, we must first analyze the «Efficiency Dividend» that separates the modern architect from the traditional saver.

May 2026 Capital Efficiency Comparison

| Institution Type | Target APY | Technology Stack | Security Framework | 5-Year Net Result (on $100k) |

| Legacy Commercial Bank | 0.45% | ACH (3-5 days) | SMS-2FA | $102,270 |

| Standard Online HYSA | 3.85% | ACH (1-2 days) | App-based MFA | $120,770 |

| Elite 2026 Smart Vault | 5.45% | Instant (RTP) | Multi-Biometric | $130,410 |

| T-Bill Ladder (Digital) | 4.10% | T+1 Settlement | Sovereign Ledger | $122,250 |

An Elite Smart Vault provides nearly $28,000 more than a legacy account over a five-year horizon. This is wealth created solely through structural optimization, effectively granting yourself an annual raise without increasing your labor output. You can track the latest verified rate movements through Bankrate’s HYSA Index.

2. The Strategy: Implementing the «Autonomous Waterfall»

The most successful financial architects of 2026 no longer move money manually. Instead, they build Autonomous Waterfalls. This is a logic-based system where capital flows through specific «pressure valves» based on real-time needs and long-term targets.

The Blueprint for a Modern Reservoir:

- The Catchment (Transactional Account): All income streams—salary, dividends, or freelance payments—land here initially. You maintain a «Survival Buffer» of exactly one month’s expenses to cover immediate liabilities.

- The Pressure Valve (RTP Sweep): Any capital exceeding your buffer is instantly siphoned using Real-Time Payment (RTP) rails into your primary High-Yield Savings Account (HYSA). This ensures you capture every possible hour of interest. Learn more about how The Clearing House RTP network is changing liquidity.

- The Smart Partitioning (Sub-Vaults): Once inside the engine, AI-driven labels partition the funds into distinct buckets:

- The Survival Core: A fortress of 6 months of absolute living expenses.

- The Tax Shield: Automated sequestration of funds based on the latest IRS 2026 Tax Guidelines.

- The Opportunity Fund: Liquid «dry powder» held in reserve to capitalize on sudden market volatility.

3. Real Yield: Protecting Purchasing Power

In the 2026 economy, nominal interest is a vanity metric. To understand your true financial progress, you must prioritize Real Yield—the difference between your APY and the Consumer Price Index (CPI).

- The Legacy Trap: If inflation is 3.4% and your bank pays 0.45%, your Real Yield is -2.95%. Your purchasing power is decaying daily.

- The Smart Pivot: At a 5.45% APY, your Real Yield is +2.05%.

A positive Real Yield is the fundamental requirement for long-term wealth building. If your savings engine is not outperforming inflation, your «safety net» is a melting ice cube.

4. Security 4.0: Defending Capital Sovereignty

As AI becomes more sophisticated, the security of your yield engine is paramount. Smart Savings in 2026 relies on Behavioral Telemetry. Rather than just checking a password, your vault monitors the unique «rhythm» of your digital interactions—typing speed, device angle, and habitual transaction patterns—to verify identity.

Furthermore, elite vaults utilize Multi-Bank Sweep Networks. This technology automatically distributes your balance across a network of FDIC-insured institutions, providing millions of dollars in federal protection while maintaining a single, unified interface. You can verify your institution’s status via the FDIC BankFind Suite.

5. Psychological Fortification: The Friction Benefit

While 2026 technology emphasizes speed, the human element still requires Intentional Friction. A smart architecture separates your «Spending Capital» from your «Investment Capital» by placing them in different institutions.

Behavioral studies frequently cited by industry experts at Investopedia demonstrate that this separation reduces «lifestyle creep.» The 30-second delay required to switch apps and move money is often enough to deactivate impulsive spending centers in the brain, protecting your future self from your present whims.

6. Optimization for the Digital Age: AI-Powered Savings

In 2026, the most advanced Smart Savings accounts are no longer passive. They are integrated with AI agents that monitor your spending patterns and local economic shifts. This creates a «Predictive Liquidity» model where your yield engine anticipates your cash flow needs.

The Agentic Advantage:

- Dynamic Rebalancing: If the AI detects a peak in market interest rates elsewhere, it prompts you to shift a portion of your «Opportunity Fund» into temporary 3-month CD ladders or T-Bills to capture a 0.25% spread.

- Subscription Siphoning: The engine identifies underused recurring payments and automatically diverts that amount into a «Compounding Bonus» sub-vault.

- Smart Tax Harvesting: By communicating with your brokerage account, the AI calculates if interest gains can be offset by realized losses, optimizing your net-after-tax yield in real-time.

7. The Global Perspective: Currency Diversification

As we progress through 2026, many Smart Yield Engines now allow for Multi-Currency Vaulting. For the sophisticated architect, this means holding a percentage of your liquid reserves in stable, high-yield digital currencies or international sovereign-backed assets.

This diversification acts as a secondary hedge against local currency devaluation. By maintaining a global liquidity footprint, you ensure that your «Smart Savings» are not tethered to the political or economic cycles of a single nation. This is the ultimate form of capital sovereignty.

8. Implementation Protocol for May 2026

To transition your current financial state into an Intelligent Yield Engine, follow these four foundational steps:

- Conduct a Latency Audit: Identify every dollar currently earning less than the current inflation rate of 3.4%.

- Select a «RTP-Native» Partner: Ensure your chosen bank is a member of the modern real-time payment networks to eliminate the hidden cost of transfer lag. Check comparisons on NerdWallet for speed ratings.

- Deploy the Waterfall: Set up your automated «sweep» rules to move excess cash every Friday at the close of business.

- Activate Biometric Layering: Move away from SMS-based 2FA and enable behavioral telemetry to harden your vault against AI-driven phishing.

9. Conclusion: The Sovereign Mandate

The 2026 economy does not forgive passivity. The «Inertia Tax» is a real and heavy burden on those who fail to adapt to the new speed of money. Building a Smart Yield Engine is about more than chasing a higher interest rate; it is about creating a secure, autonomous, and mathematically optimized fortress for your wealth.

By adopting this architecture, you claim Capital Sovereignty. You ensure your money works as hard as you do, protected by the most advanced technology of the era. The era of the «saver» is over; the era of the Financial Architect has begun.